融资融券对日历效应的影响:来自中国股票市场的实证数据

王璐

摘 要:过去的研究表明,中国股市的运行效率受到政府监管与干预并存在非对称交易的现象。2010年3月31日,中国股票市场实行了融资融券交易试点,允许投资者进行双边交易。本文显示了中国股票市场的融资融券交易如何影响2004~2016年间中国股市的日历效应。本文通过修正的AR-GARCH模型进行检验,发现收益与波动率在融资融券推出前后期间都存在显著的日历效应。在融资融券交易实施前,中国证券市场的收益率出现了显著的“正星期一”和“正星期三”效应。然而,在融资融券推出后,中国证券市场显示出显著的“负星期四”效应和“正星期五”效应。数据检验结果还表明,信息传递和市场效率在融资融券交易推出后有一定程度的提高。文章在最后针对此现象提出一些指导性决策原则。

Abstract:The efficiency of the Chinese stock market is limited by government regulation and intervention as well as the presence of asymmetries identified in previous studies. On March 31, 2010, the Chinese equity market implemented a margin trading mechanism that allowed investors to trade bilaterally. This paper shows how margin trading in the Chinese equity market affected the calendar effect for the period 2004 to 2016. Using the Modified AR-GARCH model, this paper shows that the calendar effect was statistically significant, for both return and volatility, both before and after the introduction of margin trading. The Chinese securities market witnessed a form of high Monday and high Wednesday returns before the margin trading mechanism. With margin trading, however, a significant negative Thursday effect and a positive Friday effect were observed. Other evidence indicates that information transmission and market efficiency improved to some extent over the course of the study period. The guidelines of decision marking are provided at the end of this paper.

關键词:日历效应;融资融券;修正AR-GARCH模型;中国证券市场;有效市场假说

Key words:Calendar effect; margin trading; modified AR-GARCH model; Chinese security market;

efficient market hypothesis

文章编号:1004-7026(2018)03-0142-07 中国图书分类号:F832.51;F224 文献标志码:A

INTRODUCTION

The Efficient Market Hypothesis (EMH) argues that prices on any stock market fully reflect all available information at any particular time. Thus, no investor can obtain abnormal profits by using market related information. But the existence of asymmetries in stock returns, known as calendar effects (weekend effect and day of the week effect), has been extensively investigated in an array of academic studies examining the validity of the Efficient Market Hypothesis (Cross, 1973; French, 1980; Lakonishok and Levi, 1982; Jaffe and Westerfield, 1985;).

The first scholar to research these “anomalies” in the stock market was Fields (1931), but it was Cross (1973) who called greater attention to these “anomalies.” After that, a variety of markets were investigated: the developed equity market, the emerging equity market, the foreign exchange market, futures markets and debt markets (Glassman, 1987; Corhy, 1995; Berument, 2007). Most importantly, Jaffe and Westerfield (1985a) pointed out that the existence of predictable market inefficiency could provide investors with opportunities to generate abnormal returns.

The search for abnormal returns is what makes the Chinese stock market so interesting. The Chinese stock market has many characteristics—institutional frameworks,investment behavior, cultural background—that make it unique. Because these characteristics differ from those of western markets, any investigation of the Chinese equity markets “anomalies” requires a continued search beyond the existing set of plausible candidates.

LITERATURE REVIEW

Despite evidence of the day of the week effect in both developed and emerging stock markets, the results differ dramatically and controversially as to the days on which abnormal returns are significant. In general, earlier empirical studies found a “negative Monday effect” and a “positive Friday effect” in the United States and the United Kingdom (see Cross [1973]; French [1980]). But scholarly work published later documented a gradual change in the calendar effect for the U.S. stock market.

Berument and Kiymaz (2001) demonstrated a day of the week effect present in the S&P 500 index. The study indicated that Monday returns were highest among the weekday and Wednesday returns were lowest. The study of Choudhary and Choudhary (2008) showed significantly higher positive returns on Thursday in the equity markets of Australia, the U.S,Japan, Switzerland and Korea. A unique comparative study of Bear and non-Bear markets for the U.S indexes, including the Dow Jones Industrial Average and the S&P 500, shows that the day of the week effect was present in both sampled markets (Boudreaux et al., 2010).

Recently, a growing number of scholars have suggested that the day of the week effect has disappeared in most securities markets. For example, Gonzalez-Perez and Guerrero (2013), investigating the U.S market for the period from 2004 to 2011, found no evidence of the day of the week effect. Confirmative findings were also reported by Carlucci (2013) who examined the main stock exchange indexes of Canada and the U.S. for the 2002-2012 period and found no evidence of the day of the week effect.

In contrast, the day of the effect in Asian and emerging stock markets presents another form of the negative “Tuesday effect” on returns in general (see Aggrawal and Rivoli [1989]). Other recent cross-country studies indicate that asymmetry, and especially market volatility asymmetry, was a common characteristic in the common European market index; however, the results also presented diversified patterns (Nghiem et al., 2012).

But, to be fair, there is no universally accepted explanation of the calendar effect either. The existing literature that does proffer an explanation tends to focus on the cost of capital (see Caporale and Gil-Alana[2011]), information disclosure (see Dellavigna and Pollet[2009]) or influence from futures market (see Faff and McKenzie [2002]).

Research studies on the Chinese stock market in this area are relatively few, and the conclusions from those studies are inconsistent. In fact, no day of the week effect pattern has been proven across all models.

Empirical investigations by Friedmann and Sanddorf-Kohle (2002) for volatility dynamics in the Chinese equity market applied different GARCH models. They found that it is the market segmentation in A-share and B-share market that causes the different dynamics and that the number of non-trading days has a significant influence on volatility. Also, volatility decreased when the price change limit was introduced. However, this finding was significant for the daily return on A-shares, but somewhat mixed for B shares.

By applying a dummy regression model, Singh (2014) investigated four emerging stock markets of Brazil, Russia, India and China (BRIC) for the period 1 January 2003 to 15 June 2013. Singhs article documented the results of a statistically significant negative return on Tuesday for the Chinese stock market.

An empirical research by Bohl, Schuppli and Siklos (2010) indicated that the appearances of the weekday effect seems to have decreased since the deregulation of the B-share markets in Shanghai and Shenzhen during the sample period of 1997 through 2001. They concluded that the Tuesday effect in the Chinese markets might not correlate with transmitted Monday effects from the U.S. markets but could correlate with ownership structure.

As can been seen from the previous literature concerning the day of the week effect on returns and volatility, the day of the week effects are a local, country specific phenomena. The estimation method and the data play a significant role in the results (Connolly, 1989). On March 31, 2010, the Chinese securities market began to implement the margin trading mechanism, which changed the traditional unilateral transaction pattern. With margin trading, investors can buy stocks on leverage and sell stocks they do not own. Transactions can be fulfilled based on the expectation of investors. Given this important regulatory change, it is necessary to examine the calendar effect by considering margin trading. The literature review indicates that a number of scholars have studied the Chinese stock markets but scholars hadnt really studied the effects of the 2010 change to margin trading.

This paper uses the Modified AR-GARCH model to investigate the calendar effect for both returns and volatility. Also, this paper compares the weekday effect before and after the introduction of margin trading and offers an explanation for the reasons behind such phenomena. The overall sample period begins on January 5, 2004 and ends on June 23, 2016, setting the time of the introduction of margin trading as the split date.

THEORETICAL MODEL

A Modified AR-GRACH model was used for this paper. Most studies test the day of the week effect on returns by simply employing the Ordinary Least Square (OLS) methodology (Singh, 2014, p.25; Cinko, 2015, p.101, for example). The OLS model considers dependent daily returns and independent measures of weekday dummy variables (French, 1980). Kiymaz and Berument (2003) argued that this kind of methodology, however, has two major drawbacks. First of all, the probability of autocorrelation lying in the error terms of the model might result in uncorrected interference. Secondly, the error variances in the model assume a constant variance, which may also lead to inefficient estimations.

Engle (1982) modeled the conditional variance by allowing the forecasted variance of returns to vary systematically over time. The conditional variance depends upon the squared lagged value of the error term from the previous periods of stock return. This is known as the Autoregressive Conditional Heteroskedastic model (q) [ARCH (q)]. Bollerslev (1986) developed the generalized version of the ARCH (q) and expressed the conditional variance as an extended function of lagged values of εt2 and ht2. The extended function of the ARCH model is known as General Autoregressive Conditional Heteroskedasticity (GARCH model). The GARCH models can capture the three most prominent and empirical properties of stock return data: leptokurtosis, skewness and volatility clustering.

Kiymaz and Berument (2003) included values of the return variable in the GARCH model to eliminate autoregression. Following Kiymaz and Berument, this paper used the modified AR-GRACH model accounting for both autoregression and GARCH effects.

METHODOLOGY

Four major indexes, namely, CSI300 (Shanghai-

Shenzhen 300 Index), SZSE (Shenzhen Component Index), SCI (Shanghai composite index) and SSE50 (Shanghai 50 Index) were used in this paper to test the weekly patterns. All data used in this paper were downloaded from the Wind financial terminal. The empirical analyses were carried out using Eviews 6.0. In this paper, the logs of the daily closing prices of indexes were used. The data of daily returns were constructed as the first differences of the logarithmic prices of the stock market index multiples 100. The sampled period ranges from 5 January 2004 to 23, June 2016, with 3028 observations in total for each index.

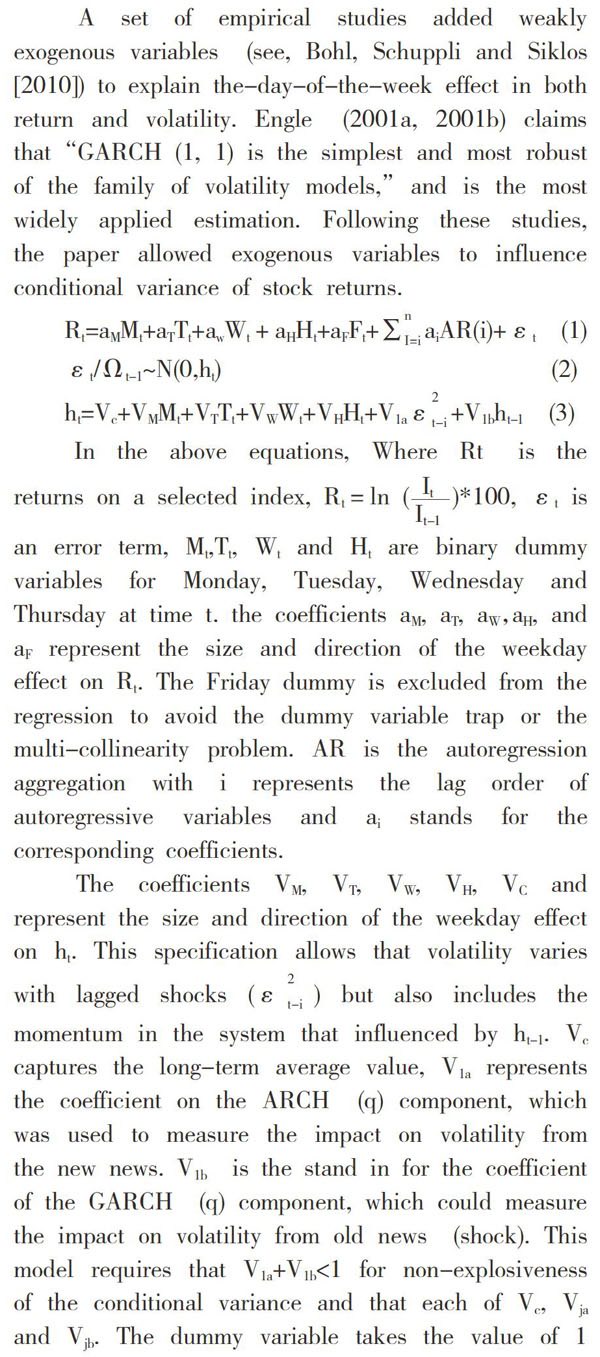

A set of empirical studies added weakly exogenous variables (see, Bohl, Schuppli and Siklos [2010]) to explain the-day-of-the-week effect in both return and volatility. Engle (2001a, 2001b) claims that “GARCH (1, 1) is the simplest and most robust of the family of volatility models,” and is the most widely applied estimation. Following these studies, the paper allowed exogenous variables to influence conditional variance of stock returns.

In this article, the Augmented Dickey-Fuller (ADF) tests were used to check the time-series property and the stochastic structure of the data series. Moreover, Levenes test was employed to test the equality of variance and variation across the day of the week.

RESULTS

The null hypothesis of a unit root tested in ADF tests for all four indexes returns series were unambiguously rejected at the 1% level of significance, suggesting all these sampled index returns were stationary. The results of the Levenes test also rejected the null hypothesis that those variances were identical through each day of the week for all index series.

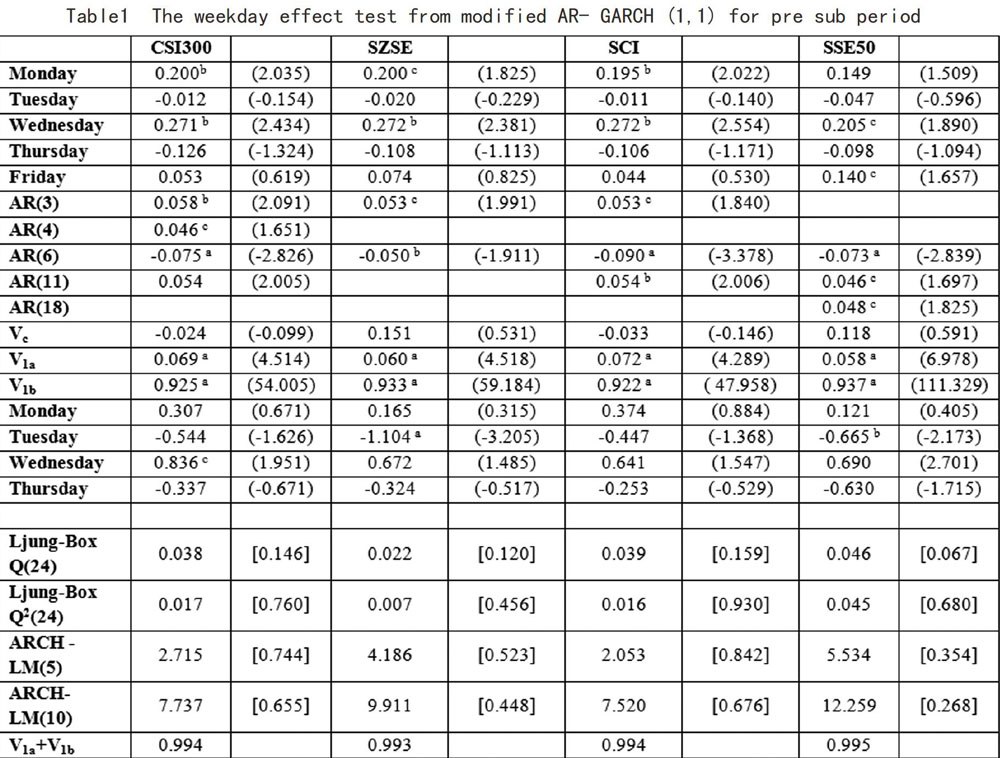

Table 1 reports results from the Modified AR-GARCH (1, 1) specification that investigated the weekday effect in stock returns and volatility for the period before the introduction of margin trading. The statistical results show that only the positive coefficient of Monday and Wednesday were statistically significant. The coefficients of Wednesday were significant at a 5% level among all indexes, and the SSE50 showed somewhat weaker evidence at the 10 per cent level on that day. The positive Monday returns were statistically significant for three of the sampled indexes but not for SSE50. The results could suggest that a positive “Monday effect” and “Wednesday effect” of return existed in Chinese stock market. The positive Monday effect might be consistent with the hypothesis (e.g. French, 1980) that the highest volatility on Monday might reflect the over-the-weekend-break shocks.

[Table 1]

When examining the calendar effect on volatility, CSI300 had the highest volatility on Wednesday, which was consistent with the highest required return on that day. By contrast, statistically significant values of the lowest volatility on Tuesday could only be found in SZSE and SSE50 index series. The ARCH coefficient and GARCH coefficient were significantly positive (at the level of 1%) for all equations, suggesting that the volatility of index return was highly persistent.

Taking the CSI300 from the pre sub period as an example,(V1a+V1b)30=0.994430=0.8450 the impact on the stock price will remain 84.50 per cent even after 30 trading days. Therefore, the abnormal fluctuation on the stock market from any shock could be very difficult to eliminate. As presented in Table 1, all coefficients in the Ljung-Box Q statistics test and Engles ARCH-LM tests provided strong support for the absence of autocorrelation and heteroscedasticity.

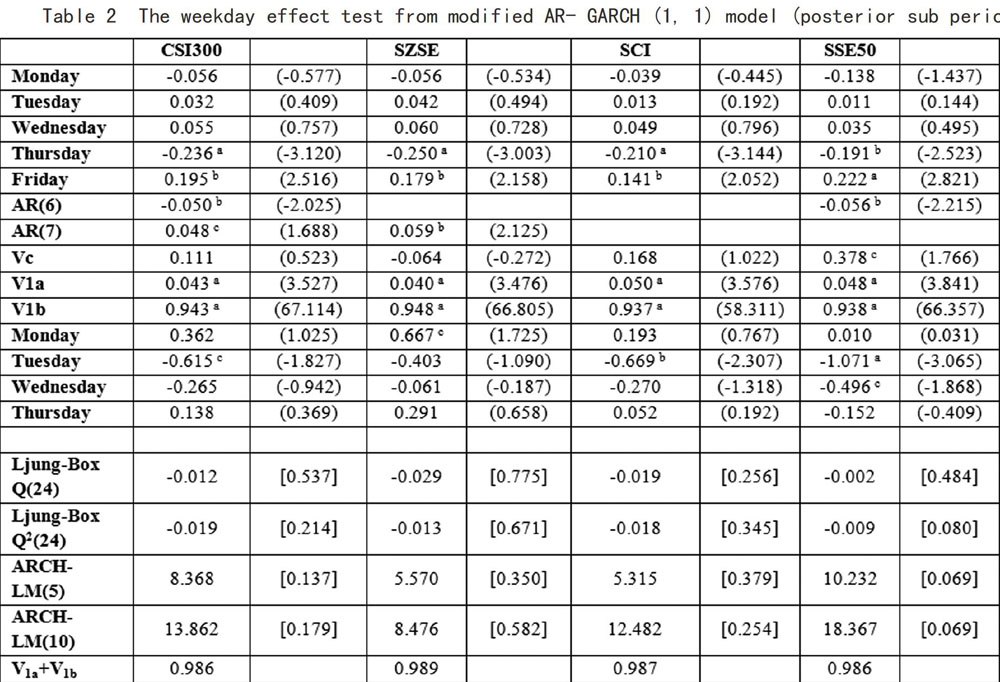

Table 2 displays the investigation of the calendar effect for the period after the introduction of margin trading. In fact, the positive “Friday effect” and the negative “Thursday effect” were both statistically significant in all four indexes. For the estimated coefficients for Thursday, CSI300, SZSE and SCI were statistically significant at the 1% level, and the critical value was 5% for SSE50. For the estimated coefficients of Friday, the critical level of Friday was statistically significant at 5% for CSI300, SZSE and SCI; SSE50 had a relatively stronger value at the 1% level.

This means the introduction of margin trading certainly changed the calendar effect in the Chinese stock market. This finding is also interesting because only a few instances of the significant lowest Thursday effect have been documented in previous studies of either the Shanghai or Shenzhen Stock Exchanges. For example, Bohl, Schuppli and Siklos (2010), while investigating stock return seasonality in B-share markets for the period 1994 to 2007 for Shenzhen A-shares and Shanghai A-shares, observed a significant Thursday effect only in the Shenzhen B-share market.

Interestingly, the risk averse assumption and the required return compensation were not reflected in the stock market with respect to volatility. According to the results of calendar effect tests on volatility, none of the indexes had the statistically significant lowest volatility on Thursday when it has the lowest return. Moreover, statistically significant negative Tuesday volatilities were found in CSI300, SCI and SSE50, but not in SZSE. The SSE50 also had significant negative volatility on Wednesday and significant positive volatility on Friday. It seems that only the highest volatility of SSE50 on Friday could explain the risk averse theory.

Another result in Table 2 shows the two parameters of the ARCH coefficient and the GARCH coefficient were less than one in all cases; both were positive and statistically significant. In fact, the sum of the two parameters is smaller than that found in the pre sub period. The impact on the stock price remained 0.986230=0.6591 after 30 trading days. This suggests that the stock market may have responded and reacted more efficiently towards the shock and news than it would have before the margin trading era.

[Table 2]

CONCLUSIONS

In conclusion, the implementation of margin trading affected the pattern of the weekday effect on returns. Before the introduction of margin trading, there was a positive Monday effect and a positive Wednesday effect in the Chinese securities market. After the implementation of margin trading, bad information could be dealt with completely through margin trading.

The market not only reacted quickly towards bad information but it also showed a higher connection with international securities. In fact, the Chinese stock market gradually manifested a weekday effect of “negative Thursday and positive Friday” that was widespread in the international securities market.

It is important that both regulators of, and investors in, the stock market focus on the weekday effect and develop corresponding regulations and trading strategies. Based on the findings in this paper, investors should pay more attention to trades on Friday but avoid trading on Thursday. Moreover, investors should pay more attention to index series trends rather than individual stocks when market risk, transaction costs and observation errors need to be taken into consideration.

REFERENCES

Aggrawal, R. and P. Rivoli. 1989. “Seasonal and day-of-the-week effects in four emerging stock markets.” Financial Review 24(4): 541-550.

Berument, H. and Kiymaz, H. 2001. “The day of the week effect on stock market volatility.” Journal of Economics and Finance 25(2): 81-93.

Berument, H., Coskun, M.N., and Sahin, A. 2007. “Day of the week effect on foreign exchange market volatility: Evidence from Turkey.” Research in International Business and Finance 21(1): 87-97.

Bohl, M.T., Schuppli, M., and Siklos, P.L. 2010. “Stock return seasonalities and investor structure: evidence from Chinas b-share markets.” China Economic Review 21(1): 190-201.

Bollerslev, T. 1986. “Generalized autoregressive conditional heteroscedasticity.”, Journal of Econometrics 31(3): 307-327.

Boudreaux, D. Rao, S., and Fuller, P. 2010. “An investigation of the weekend effect during Different Market Orientations.” Jounal of Economics and Finance 34(3): 257-268.

Caporale, G. M., and Gil-Alana, L. A. 2011. “The weekly structure of US stock Prices.” Applied Financial Economics 21(23): 1757-1764.

Carlucci, F. V., Junior, T. P. and Lima, F. G. 2013. “A Study on the day of the week effect in the four major capitals markets of the Americas.” Journal of International Finance & Economics 13(11)..

Chen, G., Kwok, C. and Rui, O. 2001. “The day-of-the-week regularity in the stock markets of China.” Journal of Multinational Financial Management, 11 (2): 139-163.

Choudhary, K. and Choudhary, S. 2008. “Day-of-the-week effect: further empirical evidence.” Asia-Pacific Journal of Management Research and Innovation 4(3): 67-74.

Cinko, M., Avci, E., Aybars, A. and Oner, M. 2015. “Analyzing the existence of the day of the week effect in selected developed country stock exchanges.” International Journal of Corporate Finance and Accounting 7 (5): 33-43.

Connolly, R. A. 1989. “An examination of the robustness of the weekend effect”, Journal of Financial and Quantitative Analysis, 24, pp. 133-169.

Corhy, A. and Fatemi, A. 1995. “On the presence of a day-of-the-week effect in the foreign exchange market.” Managerial Finance 21(8): 32-43.

Cross, F. 1973. “The behavior of stock prices on Fridays and Mondays.” Financial Analysts Journal 29: 67-69.

Dellavigna, S., and Pollet, J. M. 2009, “Investor inattention and Friday earnings announcement.” The Journal of Finance 64(2): 709-749.

Engle, R. 1982. “Autoregressive Conditional Heteroskedasticity with estimates of the variance of United Kingdom inflation.” Econometric 50(4): 987-1007.

Engle, R. and Sheppard, K. 2001a. “Theoretical and empirical properties of dynamic conditional correlation multivariate GARCH.” working paper, the National Bureau of Economic Research.1050 Massachusetts Avenue, Cambridge, October.

Engle.R. 2001b. “GARCH 101: The use of ARCH/GARCH models in applied econometrics.” Journal of Economic Perspectives 15(4): 157-168.

Faff, Robert W., and McKenzie, Michael D. 2002. “The impact of stock index futures trading on daily returns seasonality: a multicountry study.” Journal of Business 75(1): 95-125.

Fields, M. J. 1931. “Stock Prices: A problem in verification.” The Journal of Business of the University of Chicago 4(4): 415-418.

French, K. R. 1980. “Stock returns and the weekend effect.” Journal of Financial Economics 8(1): 55-69.

Friedmann, R. and Sanddorf-Kohle, W.G. 2002. “Volatility clustering and non-trading days in Chinese stock markets.” Journal of Economics & Business 54 (2): 193-217.

Glassman, D. 1987. “Exchange rate risk and transactions costs: Evidence from bid-ask spreads.” Journal of International Money and Finance 6 (4): 479-490.

Gonzalez-Perez, M. T. and Guerrero, D. E. 2013. “Day-of-the-week effect on the VIX. a parsimonious representation.” North American Journal of Economics and Finance 25: 243-260.

Jaffe, J., & Westerfield, R. 1985b. “Patterns in Japanese common stock returns.” Journal of Financial and Quantitative Analysis, 20(2): 261-272.

Kiymaz, H. and Berument, H. 2003. “The day of the week effect on stock market volatility and volume: International evidence.” Review of financial Economics 12(4): 363-380.

Lakonishok, J. and M. Levi. 1982. “Weekend effects on stock returns: a note.” Journal of Finance 37(3): 883-889.

Nghiem, L. T., Hau, L. L., Tri, H. M., Duy, V. Q., and Dalina, A. 2012. “Day-of-the-week in different stock markets: new evidence on model-dependency in testing seasonalities in stock return.” Centre for Asian Studies, CAS Discussion Paper No:85.

Singh, S. P. 2014. “Stock market anomalies: evidence from emerging BRIC markets.” Vision: The Journal of Business Perspective 18 (1): 23-28.

APPENDICES

Table 1. The weekday effect test from modified AR- GARCH (1, 1) for pre sub period

Table 2. The weekday effect test from modified AR- GARCH (1, 1) model (posterior sub period)